Philip H. Howard

Abstract: Diversity is important for the resilience of food systems, as well as for its own sake. Just how diverse are the systems that produce our food? I explore this question with a focus on wheat and bread and North America, and even more specifically in baking, milling and farming. Although the opacity of food and agricultural systems makes definitive answers difficult, these segments appear to be increasingly uniform with respect to ownership, geography, varieties and genes. There are also important countertrends, and while efforts to resist uniformity are currently small, they are making some progress in maintaining or even increasing diversity in some areas.

Keywords: Diversity, Uniformity, Ownership, Geography, Varieties, Wheat, Bread

*Pre-publication version of article published in 2016, in Agriculture and Human Values, 33(4), 953-960. Presidential address presented at the 2016 annual meeting of the Agriculture, Food and Human Values Society held at the University of Toronto Scarborough, Ontario, Canada, on June 22-25, 2016 (viewable online).

Introduction

One of the reasons that our societies (Agriculture, Food and Human Values Society; Association for the Study of Food and Society; Canadian Association for Food Studies) as well as the number of food studies programs are growing so rapidly is that food systems have become quite opaque. It is very difficult to answer many questions we have about our food, including as one example: how diverse are the systems producing what we eat? Diversity is an important value for its own sake, and it is also important for resilience. For instance, monocultures of genetically uniform organisms in food production provided favorable conditions for potato blight in Ireland in the mid-1800s, corn blight in the United States and Canada in 1970, and in more recent years, avian influenza in Asia and North America.

Characterizing diversity is an important task for interdisciplinary food scholars. Our findings may help raise awareness of the often hidden risks of inadequate levels of diversity. In addition, sharing these findings with the public has the potential to assist efforts to address these problems, and to move toward more resilient food systems. In recent years we have seen not only greater public interest in the food system, but more collective actions to demand change. This has resulted in notable successes, such as the reduction of antibiotic usage in farm animals, the removal of certain synthetic ingredients from many processed foods, and improved wages and working conditions for some U.S. tomato farm laborers (Howard 2016).

We often think of diversity or uniformity in on-farm, biological terms, such as the factors that contributed to the epidemics noted above. I am a member of the International Panel of Experts on Sustainable Food Systems (iPES-Food), which recently released a report titled, “From Uniformity to Diversity: A Paradigm Shift From Industrial Agriculture to Diversified Agroecological Systems” (2016). This report compares types of farming systems, such as organic and conventional, and identifies differences in: (1) genes, (2) varieties & breeds and (3) the number of species in agricultural production. To this list of on-farm attributes we could add (4) time, such as increasingly uniform planting and harvesting of field crops.

Such on-farm attributes are extremely important, but we could also broaden this list to include off-farm and social attributes of the food system, including (5) ownership, (6) location or geography and (7) the number of ingredients in our foods and diets. These may also be very significant for food system resilience. As one example, in 2010, only as a result of a recall, did we learn that just two farms, in one county in Iowa, were supplying eggs to at least 22 states—these were repackaged at half a dozen locations and sold under more than 40 different brands. When the feed supplies at these geographically concentrated operations were contaminated, it led to an epidemic that sickened thousands of people, and resulted in a recall of more than half a billion eggs (Howard 2010).

The Republican governor of Iowa (Terry Branstad) called Jack DeCoster, an investor who had ties to both operations, a “bad egg” among operations this size (Woodard 2015). Things can go wrong even in the best-run facilities, however, and much of the egg industry is now just as geographically uniform as DeCoster’s operations—including certified organic. Almost 20% of organic eggs in the U.S. come from one firm, Herbruck’s (Shanker 2016), which is based in Saranac, Michigan, an hour’s drive from where I live. Using Google Earth, you can see the scale of their operations, which also include conventional egg production facilities. The firm has more than 80 hen houses, each more than a football field long. Herbruck’s also supplies all of McDonald’s eggs east of the Mississippi river, and 60% of the eggs sold in Michigan. Unfortunately, eggs are not a unique case, and many other foods are becoming just as uniform in both ownership and geography (e.g. DeLind and Howard 2008).

For human diets, although thousands of plants and animal species can be used as foods, it is estimated that just wheat, corn and rice account more than half of the world’s calorie consumption from plants (FAO 1995). These products are frequently consumed in ultra-processed forms such as high fructose corn syrup and hydrogenated soybean oil. One recent estimate suggests that more than 60% of calories consumed in U.S. and Canadian diets are in the form of highly processed foods (Poti et al. 2015; Moubarac et al. 2014), which have been associated with numerous negative health outcomes (Winson 2013).

I have recently been exploring diversity and uniformity in wheat, which provides one-fifth of the world’s calories, as well as a majority of the world’s protein. As you also know, bread is so significant in many cultures that it is often used as a generic term for food. Numerous metaphors reference its importance, such as bread-winners and dough (Halloran 2015). I have focused specifically the systems that supply us with bread in North America. Because these can be very complex, I only discuss three key stages: (1) baking, (2) milling and (3) wheat farming—thus omitting a number of additional actors, including brokers, distributors and retailers (Galli et al. 2015).

Baking

The baking segment in North America has changed quite dramatically from the 1890s. At that time, 90% of bread was homemade, and made mostly by women. By 1930, however, 90% of bread came from factories, and was made mostly by men (Bobrow-Strain 2012). One of the key players in this transformation was William Ward. Ward’s grandfather and great-grandfather moved to the U.S. from Ireland in 1849 (during the potato blight), and eventually grew a small bakery in Pittsburgh into a large, industrial operation. William Ward attempted to go further, though, using funding and strategies from steel barons to create a bread trust (Bobrow-Strain 2012). In 1925, he acquired the maker of Wonder Bread, which was the largest bakery in the U.S.

His plans ultimately failed in 1926 when President Coolidge’s administration refused to allow the combination of the Ward, Continental and General baking companies. A few years later Ward Baking Company was renamed Wonder, and as one of the first breads to be sold pre-sliced in the 1930s, as well as enriched in the 1940s, the firm remained dominant for decades. Wonder was acquired several times by even larger corporations, however, before going bankrupt in 2009 (Green and Timberlake 2012).

Today, with a much larger population, the situation is remarkably similar. The two leading firms controlled 49% of the U.S. bread market in 2012 (Sosland 2013), and both reported increasing their market share in subsequent years. Therefore, in terms of ownership, the majority the bread now sold in the U.S. is from this duopoly—the Coke and Pepsi of bread. Grupo Bimbo is based in Mexico, and Flowers Foods is headquartered in Georgia. In distant third place is the Campbell Soup Co. with an estimated 7.5% of the market (Sosland 2015).

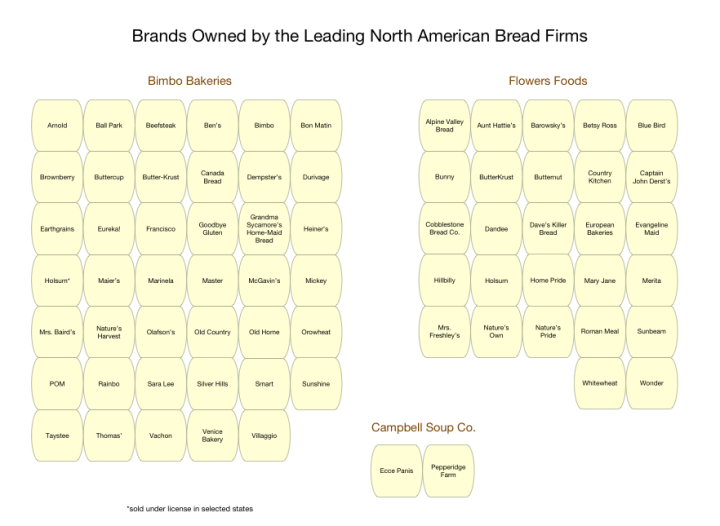

The store shelves, however, don’t appear as uniform as cola, because each has dozens of brands, which helps to maintain an illusion of choice for consumers. Grupo Bimbo alone has more than 100 brands and 10,000 different products globally. Figure 1 shows some of the firm’s key bread brands in North America, which include Brownberry, Canada Bread, Earthgrains, Orowheat, Nature’s Harvest and Sara Lee. Flowers also has several dozen bread brands, as well as snack brands like Tastykake, and tortilla brands such as MiCasa. Its bread brands include Butternut, Nature’s Own, Nature’s Pride, Home Pride and Roman Meal. Campbell Soup Company’s primary bread brand is Pepperidge farm, but it too controls numerous others, particularly for the broader category of baked goods (e.g. the Danish butter cookie brands Royal Dansk, Kjeldsens, Riberhus, Denmark, Copenhagen and Ripensa of Denmark).

Figure 1. Brands owned by the leading North American bread firms (see above; click for pdf version)

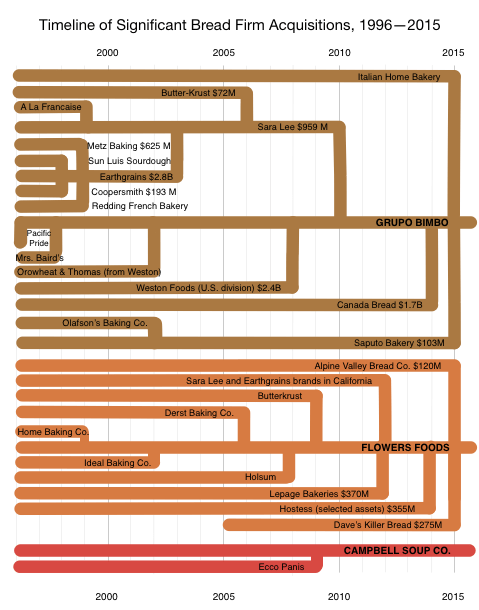

How did these companies end up controlling so many brand names? Acquisitions played a key role. Figure 2 is a timeline beginning twenty years ago, showing more than two-dozen bread bakeries that were incorporated into Bimbo and Flowers. To give you an idea of how complicated these ownership relations have become, the brand Wonder is now owned by Flowers in the U.S., Bimbo in Mexico, and George Weston in Canada. Some of the most recent strategic moves involve certified organic brands. In 2015, Flowers acquired Dave’s Killer Bread for $275 million and Alpine Valley Bread Company for $120 million, and Bimbo began nationally distributing its Eureka! brand organic bread in the following year.

Figure 2. Timeline of significant bread firm acquisitions (click for pdf version)

With regard to geography, bread is quite perishable, so firms cannot rely on just one large bakery to distribute to an entire continent. The number of locations has declined, however, as ownership consolidated. Bimbo closed 18 plants in the years following its acquisition of Sara Lee, and added just 2 (Sosland 2014). Bimbo currently has 70 bakeries in the U.S., and Flowers has 49 (Flowers Foods 2016). In other words, more than half the bread sold in fifty states is produced in little more than one hundred locations. For comparison, in 1920 just 27% of sales came from 800 plants (Alsberg 1926).

Milling

One hundred and fifty years ago most flour mills were relatively small, and frequently located near a stream that could power a waterwheel. In 1870 there were 22,573 mills in the U.S (Posner and Hoseney 2015). The industry became much more concentrated after the Civil War though, both geographically and in ownership. This change was influenced by new technologies, which included new sources of power and transportation, along with an industrial milling process developed in Hungary, which made flour less perishable.

Within a few decades, the precursors of General Mills, Pillsbury and another Minneapolis firm (Northwestern Consolidated) dominated the industry with just two-dozen mills. By 1898 they were described as a “flour trust,” but their power declined soon afterword as wheat production increased in other parts of the continent, including Ontario and Quebec (Millikan 2003).

As with baking, however, the current situation is moving towards greater uniformity of ownership. During the 1980s, the market share of the top four firms increased from 40 to 61% (Heffernan and Hendrickson 2002), and remains very high. According to the North American Miller’s Association, 95% of the industry’s capacity is controlled by its 48 member firms, which together have 170 mills (NAMA 2011). The top two firms, however, control more than one-third of these facilities.

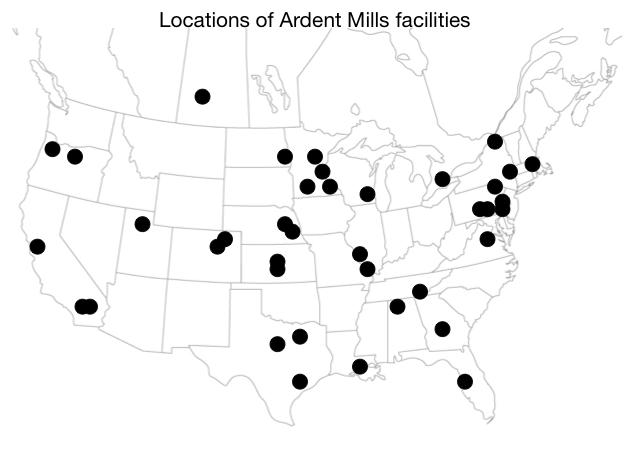

The largest is Ardent Mills, which is a joint venture formed in 2014 to combine the operations of privately held Cargill, publicly traded ConAgra Brands, and the farmer cooperative CHS. Cargill and ConAgra each have a 44% stake, with the remaining 12% owned by CHS (formerly Cenex Harvest States, as a result of a merger between two large farmer cooperatives). As Figure 3 indicates, Ardent Mills currently has 40 mills in the U.S. and Canada, including one in the Toronto metropolitan area that was acquired from Mondelez. Although the U.S. Department of Justice required the sale of another four facilities to approve the merger, Ardent Mills now owns the majority of mills in some regions of the continent—this gives farmers fewer options to sell their crops, and bakeries fewer options to buy flour. The firm is estimated to control more than 34% of the flour market in the U.S. (Runyon 2013).

Figure 3. Locations of Ardent Mills facilities

Archer Daniels Midland (ADM) is the second largest miller in the U.S., with 17% of sales. It would have been ranked first if the Ardent Mills merger had not been approved. ADM is infamous for its internal slogan, “the competitor is our friend and the customer is our enemy,” as well the conviction of its executives for fixing prices in lysine and citric acid markets (Lieber 2000, p. 10). The firm has 23 wheat mills in the U.S. and 6 in Canada, although it shut down additional mills in Missouri in 2010, and Alberta in 2013.

Some of the problems with such geographic concentration became evident this year. On May 31, General Mills announced a voluntary recall of flour milled at its Kansas City, MO plant, due to concern it was linked to outbreak of E. coli O121 and O26 in 21 states. At least 46 people are suspected of contracting the illness from consuming the flour in raw form (CDC 2016).

Farming

Farming is a bit more complicated. Wheat cannot yet be produced in a factory, therefore it must be planted in the ground. This makes it much more extensive geographically than the downstream segments of milling and baking. Globally, the leading producers are the European Union, China and India, followed by U.S. Russia and Canada (Statista 2016). The U.S. was once the world’s leading exporter, but has recently fallen behind the E.U. and Russia. In Canada, wheat production in centered in the southern Prairie Provinces, along with southern Ontario and Quebec. This crop is grown in most states in the U.S., but is concentrated in the Great Plains and eastern Washington and Oregon.

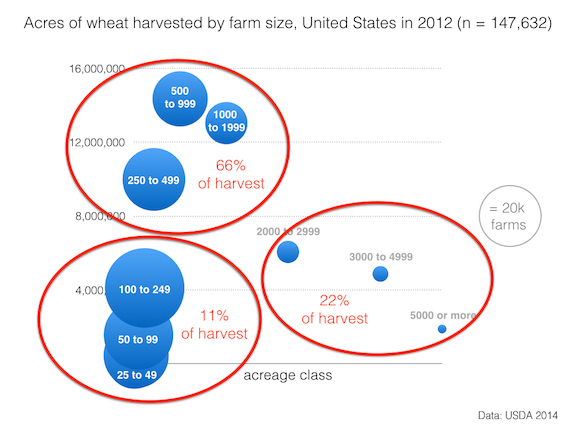

Wheat accounted for 55 million acres harvested in the U.S. in 2012, and was exceeded in extent only by corn and soybeans. The USDA census of agriculture data reported that there were more than 147,000 farms that contributed to this production, although the number of farms is declining as their average size increases. For example, from 1987 to 2007 the median acres of wheat harvested more than doubled, rising from 404 to 910 (MacDonald, Korb, and Hoppe 2013). Figure 4 shows that the middle categories (43,000 farms of 250 to 1,999 acres in size) accounted for two-thirds of the harvest in 2012. A much lower percentage of the harvest, 11%, came from smaller farms (nearly 101,000 farms with less than 250 acres).

Figure 4. Acres of wheat harvested by farm size in the United States

Wheat can be used for many food products, and this is reflected in the extent of the six major classes that are grown in North America. In the U.S., approximately 40% is hard red winter, meaning it is planted in the fall and resumes growing in the following year, and 20% is hard red spring, which is planted in the spring and harvested the same year—both are most commonly used for bread. The rest is planted in soft red winter, soft white, hard white and durum varieties—these are more typically processed into cookies, crackers, cakes, pastries, pasta, etc. (Bond and Liefert 2016). Hard red spring is the most common class of wheat in Canada. Handling systems for collecting wheat have typically focused on these classes, rather than specific varieties (Magnan 2011).

The number of varieties planted in North America has narrowed substantially in the last century. There are at least 25 species (Rogosa 2016), and over 30,000 varieties of wheat, which is not surprising when you consider it is a crop that has been cultivated for approximately 10,000 years. In Michigan, however, just six varieties are planted on half the acreage (Nagelkirk and Black 2012), and most other states report similar patterns of uniformity. When evaluating the diversity of genes within these varieties, the science is quite complicated, but most researchers suggest that in North America it narrowed from 1930 to 1980. This trend was reversed beginning in the 1980s, due to public and plant breeder concerns for future food security, such as the threat of wheat stem rust (Reif et al. 2005; Fu and Somers 2009). More recent research in France, which integrated both genetic and spatial data, however, suggests that wheat genetic diversity in that country began to decline again in the 1990s (Bonnin et al. 2014).

Seed saving is more common for wheat than other major commodities, such as corn and soybeans (Mascarenhas and Busch 2006), therefore there is greater potential knowledge and infrastructure to increase diversity. Major seed/chemical corporations—including Bayer, Syngenta and DuPont—have been investing in the development of hybrid varieties of wheat for decades, however. The effort is biologically challenging, but if they achieve their claims that they will be commercially successful within the next few years, rates of seed saving are likely to decline further (Kloppenburg 2004).

Resistance

Although the dominant trends are toward uniformity, there are also numerous forms of resistance. The motivations behind these efforts are varied, but they may have the effect of maintaining diversity, whether or not it is an explicit goal. “Bake like it’s 1869,” for example, is a slogan of GRAINSTORM Heritage Baking in Toronto (2016). Their vision, shared by a new wave of local bakeries, is to grow an alternative to the industrial white flour bread system.

There are also strong movements to reduce wheat consumption, or even give it up entirely, such as those who have adopted gluten-free diets, due to sensitivity to this protein. However, some people report that they are able to tolerate less common varieties of wheat, which has in turn contributed to rapidly rising production of so-called ‘ancient’ or ‘heritage’ wheat varieties. These include einkorn, emmer, Turkey Red, Red Fife and spelt—varieties that were more frequently planted in the early 1900s. The demand for ancient and heritage wheat varieties is also driven by interest in nutrition and better tasting bread (Fromartz 2015). For example, Kamut is a name brand for the flavorful, nutty tasting khorasan variety of wheat, which is grown on more than 1,200 farms in Canada and the U.S.—much of the harvest is currently exported to customers in Italy (Hassanein 2011). The price premiums for ancient and heritage varieties may result in higher returns per acre for farmers, despite lower yields than more modern varieties (Montana Flour & Grains 2016).

The systems that involve less common wheat varieties typically reduce the number of links in the supply chain, often by design. It is remarkable that interest in regional food systems is now extending to wheat, even though it has the disadvantage of being a commodity with a low ratio of value to volume (Hills, Goldberger, and Jones 2013). Regional supply chains are more resilient to disruptions, such as those caused by natural disasters (Paci-Green and Berardi 2015), although these positive externalities are not currently reflected in prices. Even for longer supply chains (such as Kamut), less concentrated ownership is likely to lead to more diverse organizational forms, greater decision-making autonomy, and a greater capacity to adjust to change (Hendrickson 2015; Rotz and Fraser 2015).

Another aspect that is critical for resilience is knowledge, which industrial systems have made less accessible (Anderson 2015), particularly when it contributes to greater self-reliance. In reaction, movements to regain once common skills, such as baking bread, are on the upswing. Some home bakers are even going further and milling their own flour at home. Their motivations include better flavor, texture and nutritional differences—stone ground flour has more vitamin A and B1 (thiamin) than flour from a roller mill. For those who are not grinding wheat themselves, more options are being provided by an increasing number of small-scale stone mill operations—these include renovated 1800s era mills, such as Westwind Milling in Linden, Michigan. One of the most successful stone-grinding operations in North America is Bob’s Red Mill, and you can now find this company’s spelt flour in nearly any supermarket.

Another example of how mainstream these trends have become is illustrated by Wegmans, a chain of 91 supermarkets headquartered in Rochester, New York (which was called “flour city” in the early 1800s). One nearby Wegmans location recently started selling bread made from regionally sourced einkorn and rye, freshly milled and baked in the store. The baker, Nick Greco, was formerly an instructor at the Culinary Institute of America. He brought his own small electric mill into the store, and provided the CEO a taste of bread made from freshly ground flour. A few weeks later Greco was on a plane to Austria, to explore buying the stone mill that was eventually brought to the store (Schuhmacher 2016).

If that is not mainstream enough for you, both General Mills and the Kellogg Company have introduced breakfast cereals that prominently feature “ancient grains” on the label, and contain the ingredients Kamut and spelt (along with quinoa). You might wonder if the motivation was to increase the diversity of the food supply, or perhaps the purported health benefits. Instead, after criticism of the much higher amounts of sugar in “Cheerios + Ancient Grains” when compared to regular Cheerios, marketing manager Alan Cunningham explained that General Mills, “simply wanted to capitalize on the ancient-grains trend while also making the cereal taste good” (Vara 2014, n.p.). So you can see that although smaller firms are increasing the diversity of options in ways that resonate with greater numbers of people, larger firms are quick to co-opt the most successful efforts. This may not be entirely bad, however, if it results in increased plantings of less common wheat varieties (Longin and Würschum 2016), and greater accessibility for those of us who live in areas that are not on the leading edge of food trends.

Summary and conclusion

I explored uniformity and diversity in three parts of the North American wheat/bread chain: baking, milling and farming. These segments appear to be increasingly uniform with respect to ownership, geography, varieties and genes. There are also important resistance efforts, however, and although these are currently small, they are making some progress in maintaining or even increasing diversity in some areas.

Many questions remain to be answered on this topic, but I conclude with three: (1) What would it look like if we all put on our food detective caps, and decoded diversity and uniformity, not just in bread and wheat, but in a number of other food systems? (2) How might we communicate this information to the public, so that people are better informed about the values they are currently supporting? (3) What contribution might this make to increasing diversity in food systems as a result?

References

Alsberg, C. 1926. Combination in the American bread-baking industry: with some observations on the mergers of 1924-25. Stanford University, CA: Stanford University Press.

Anderson, M.D. 2015. “The role of knowledge in building food security resilience across food system domains.” Journal of Environmental Studies and Sciences5(4): 543–59.

Bobrow-Strain, A. 2012. White bread: a social history of the store-bought loaf. Boston, MA: Beacon Press.

Bond, J.K., and O. Liefert. 2016. “Wheat: background.” Washington, DC: USDA Economic Research Service, June 30. http://www.ers.usda.gov/topics/crops/wheat/background.aspx.

Bonnin, I., C. Bonneuil, R. Goffaux, P. Montalent, and I. Goldringer. 2014. “Explaining the decrease in the genetic diversity of wheat in France over the 20th century.” Agriculture, Ecosystems & Environment 195: 183–92.

CDC. 2016. “Multistate outbreak of Shiga toxin-producing Escherichia coli infections linked to flour.” Atlanta, GA: Centers for Disease Control, July 25. http://www.cdc.gov/ecoli/2016/o121-06-16/index.html.

DeLind, L.B., and P.H. Howard. 2008. “Safe at any scale? food scares, food regulation, and scaled alternatives.” Agriculture and Human Values 25(3): 301–17.

FAO. 1995. “Dimensions of need: an atlas of food and agriculture.” Santa Barbara, CA: Food and Agriculture Organization of the United Nations.

Flowers Foods. 2016. “Flowers Foods investor fact sheet.” September. http://www.flowersfoods.com/FFC_InvestorCenter/FinancialDocuments/InvestorFactSheet/FLOInvestorFactSheet.pdf. Accessed 5 Sept 2016.

Fromartz, S. 2015. In search of the perfect loaf: a home baker’s odyssey. New York: Penguin Publishing Group.

Fu, Y.-B., and D.J. Somers. 2009. “Genome-wide reduction of genetic diversity in wheat breeding.” Crop Science 49(1): 161–168.

Galli, F., F. Bartolini, G. Brunori, L. Colombo, O. Gava, S. Grando, and A. Marescotti. 2015. “Sustainability assessment of food supply chains: an application to local and global bread in Italy.” Agricultural and Food Economics 3(1).

GRAINSTORM. 2016. “GRAINSTORM Heritage Baking.” http://www.grainstorm.com/. Accessed 25 May 2016.

Green, J., and C. Timberlake. 2012. “Innovation long in mix for hostess brands.” San Francisco Chronicle, November 21.

Halloran, A. 2015. The new bread basket: how the new crop of grain growers, plant breeders, millers, maltsters, bakers, brewers, and local food activists are redefining our daily loaf. White River Junction, VT: Chelsea Green Publishing.

Hassanein, N. 2011. “Values-based supply chains and the case of Kamut.” Appetite 56(2): 531.

Heffernan, W.D., and M.K. Hendrickson. 2002. “Multi-national concentrated food processing and marketing systems and the farm crisis.” Paper presented at the Annual Meeting of the American Association for the Advancement of Science Symposium: Science and Sustainability. Boston, MA.

Hendrickson, M.K. 2015. “Resilience in a concentrated and consolidated food system.” Journal of Environmental Studies and Sciences 5(3): 418–31.

Hills, K.M., J.R. Goldberger, and S.S. Jones. 2013. “Commercial bakers and the relocalization of wheat in western Washington State.” Agriculture and Human Values 30(3): 365–78.

Howard, P.H. 2010. “Four ways to regain control of your food.” Yes Magazine, October 11. http://www.yesmagazine.org/planet/4-ways-to-regain-control-of-your-food.

Howard, P.H. 2016. Concentration and power in the food system: who controls what we eat? London: Bloomsbury Academic.

iPES-Food. 2016. “From uniformity to diversity: a paradigm shift from industrial agriculture to diversified agroecological systems.” International Panel of Experts on Sustainable Food Systems. http://www.ipes-food.org/images/Reports/UniformityToDiversity_FullReport.pdf.

Kloppenburg, J.R. 2004. First the seed: the political economy of plant biotechnology. Madison, WI: University of Wisconsin Press.

Lieber, J.B. 2000. Rats in the grain: the dirty tricks and trials of Archer Daniels Midland, the supermarket to the world. New York: Four Walls Eight Windows.

Longin, C.F.H., and T. Würschum. 2016. “Back to the future – tapping into ancient grains for food diversity.” Trends in Plant Science 21(9): 731–37.

MacDonald, J.M., P. Korb, and R.A. Hoppe. 2013. “Farm size and the organization of U.S. crop farming.” Economic Research Report 152. USDA Economic Research Service.

Magnan, A. 2011. “Bread in the economy of qualities: the creative reconstitution of the Canada-UK commodity chain for wheat.” Rural Sociology 76(2): 197–228.

Mascarenhas, M., and L. Busch. 2006. “Seeds of change: intellectual property rights, genetically modified soybeans and seed saving in the United States.”Sociologia Ruralis 46(2): 122–38.

Millikan, William. 2003. A union against unions: the Minneapolis Citizens Alliance and its fight against organized labor, 1903-1947. St. Paul, MN: Minnesota Historical Society Press.

Montana Flour & Grains. 2016. “Opportunity for farmers: consumer demand produces premium markets.” http://www.montanaflour.com/about-us/opportunity-for-farmers/. Accessed 22 May 2016.

Moubarac, J.-C., M. Batal, A.P.B. Martins, R. Claro, R.B. Levy, G. Cannon, and C. Monteiro. 2014. “Processed and ultra-processed food products: consumption trends in Canada from 1938 to 2011.” Canadian Journal of Dietetic Practice and Research 75(1): 15–21.

Nagelkirk, M., and R. Black. 2012. “Wheat varieties used in Michigan.” MSU Extension, February 1. http://msue.anr.msu.edu/news/wheat_varieties_used_in_michigan.

NAMA. 2011. “Wheat milling process.” Arlington, VA: North American Millers’ Association. http://www.namamillers.org/education/wheat-milling-process/. Acccessed 15 May 2016.

Paci-Green, R., and G. Berardi. 2015. “Do global food systems have an Achilles heel? the potential for regional food systems to support resilience in regional disasters.” Journal of Environmental Studies and Sciences 5(4): 685–98.

Posner, E.S., and R.C. Hoseney. 2015. “A century of advances in milling and baking.” Cereal Foods World 60(3): 148–53.

Poti, J.M., M.A. Mendez, S.W. Ng, and B.M. Popkin. 2015. “Is the degree of food processing and convenience linked with the nutritional quality of foods purchased by US households?” American Journal of Clinical Nutrition 101(6): 1251–62.

Reif, J.C., P. Zhang, S. Dreisigacker, M.L. Warburton, M. van Ginkel, D. Hoisington, M. Bohn, and A.E. Melchinger. 2005. “Wheat genetic diversity trends during domestication and breeding.” Theoretical and Applied Genetics 110(5): 859–64.

Rogosa, E. 2016. Restoring heritage grains: the culture, biodiversity, resilience, and cuisine of ancient wheats. White River Junction, VT: Chelsea Green Publishing.

Rotz, S., and E.D.G. Fraser. 2015. “Resilience and the industrial food system: analyzing the impacts of agricultural industrialization on food system vulnerability.”Journal of Environmental Studies and Sciences 5(3): 459–73.

Runyon, L. 2013. “Proposed merger would create flour milling Goliath.” Harvest Public Media, November 13. http://harvestpublicmedia.org/article/proposed-merger-could-create-flour-milling-goliath-wheat.

Schuhmacher, T. 2016. “Wegmans unveils new mill in Pittsford store.” Rochester Democrat and Chronicle, February 2. http://www.democratandchronicle.com/story/lifestyle/food-and-drink/2016/02/02/wegmans-unveils-new-mill-pittsford-store/79648956/.

Shanker, D. 2016. “Egg comes first in fight over what it means to be organic.” Bloomberg, May 19. https://www.bloomberg.com/news/articles/2016-05-19/egg-comes-first-in-fight-over-what-it-means-to-be-organic.

Sosland, J. 2013. “Flowers sees no lack of competition in baking.” BakingBusiness.com, March 25. http://www.bakingbusiness.com/articles/news_home/Business/2013/03/Flowers_sees_no_lack_of_compet.aspx.

Sosland, J. 2014. “Bimbo sees more plant closings in 2014 and beyond.” BakingBusiness.com, February 24. http://www.bakingbusiness.com/articles/news_home/Business/2014/02/Bimbo_sees_more_plant_closings.aspx.

Sosland, J. 2015. “Vying for a new generation.” Milling & Baking News, March 17.

Statista. 2016. “Principal exporting countries of wheat flour and products.” New York: Statista. http://www.statista.com/statistics/190429/principal-exporting-countries-of-wheat-flour-and-products/. Accessed 8 May 2016.

USDA. 2014. “2012 Census of Agriculture.” Washington, DC: US Department of Agriculture, National Agricultural Statistics Service.

Vara, V. 2014. “Why we’re willing to pay more for cereals with ancient grains.” The New Yorker, October 24. http://www.newyorker.com/business/currency/well-pay-ancient-grains-cheerios.

Winson, A. 2013. The industrial diet: the degradation of food and the struggle for healthy eating. Vancouver, BC: UBC Press.

Woodard, C. 2015. “Notorious egg seller ‘Jack’ DeCoster gets jail time for Salmonella outbreak.” Portland Press Herald, April 13. http://www.pressherald.com/2015/04/13/maine-businessman-jack-decoster-gets-jail-for-selling-tainted-eggs/.

One thought on “Decoding Diversity in the Food System: Wheat and Bread in North America”