January 2023

Amos Strömberg, Lund University

Phil Howard, Michigan State University

While seeds have become increasingly commodified in recent decades, they still constitute the foundation of most of the world’s food supply chains. The consolidation of the agrochemical and seed industries, especially in the last few years, has thus raised a number of concerns about this growing concentration of power. Colossal changes have placed the majority of agrochemical and seed sales globally under the control of six firms by the early 2000s (Howard 2009), and subsequent “megamergers” reduced this to just four firms by 2018. These trends have blurred previously distinct boundaries between seeds, agrochemicals, and biotechnology, and more recently, between other sectors, including biologicals (“plant protection and strengthening products that are derived from or inspired by nature”) and digital agriculture (the growth of robotics, software, automation, and sophisticated data analysis in agriculture). This post focuses on the major transformations that have taken place globally in seeds and digital agriculture in the last four years—since the last update of the seed industry structure graphic in 2018.

The last four years in the global seed industry: continued concentration and the merger of giants in China

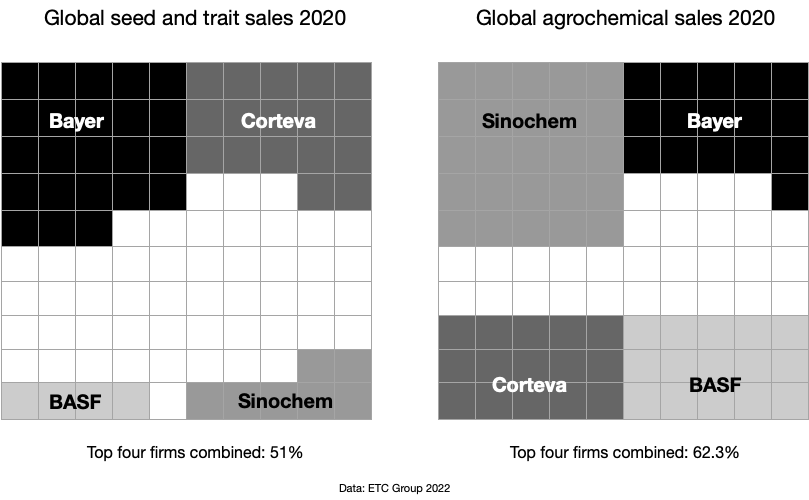

Between 2018 and 2022 the trend of global concentration and consolidation within agrochemical and seed companies has continued unhindered. The “Big Four” agrochemical firms, Bayer, BASF, Corteva and Sinochem, have all increased their power through tactical acquisitions and mergers. The megamerger of Sinochem and ChemChina in 2021 marked a notable change in the agri-food system—the combination of two giant firms owned by the government of China has led to the formation of the world’s largest chemical conglomerate and the third largest seed firm, operating under the name of a previously acquired Swiss giant, Syngenta (ETC 2022).

Within the agrochemical sector, companies produce and sell a variety of pesticides for agriculture, including insecticides, herbicides and fungicides. These are frequently tied to seeds, such as crops that have been genetically engineered to contain insecticides, or to be resistant to herbicides. In recent years, in part due increasing government and private retailer restrictions on the use of agrochemicals, giant seed-chemical firms have been investing in firms that specialize in biologicals for pest control (as well as nitrogen fixation and carbon sequestration)—the application of these products may include seed treatments. Syngenta, for example, acquired Valagro in 2020, a move said to “help farmers deliver a food system working in harmony with nature”, and now claim to be “one of the strongest players in the global biologicals market”. Other noteworthy events included Corteva acquiring the leading biologicals and biotechnology company Symborg, followed by another firm in this sector, the Stoller Group in 2022. In addition, Bayer announced a so-called biologicals “powerhouse” in 2022 by partnering with Gingko Bioworks. Fertilizer firms, such as Nutrien and Yara, are also acquiring start-ups in the biologicals sector.

Oligopoly and global market shares

Institutional economists suggest that when four firms combine to control 40 percent or more of a market it is no longer competitive (Scherer and Ross 1990; Shepard and Shepard 2004), due to the conducive environment for price signaling that may result—one firm can simply indicate that it will raise prices and the other dominant firms will benefit by following suit (Baran and Sweezy 1966). This type of control can be described as a shared monopoly, or more technically, an oligopoly. Such high levels of concentration can also threaten political sovereignty, or lead to additional consequences, including negative impacts on communities, labor, human health, animal welfare, and the environment (Howard 2021). Fuglie et al. (2011) suggested that the market share of the top four seed firms globally increased from 21 percent in 1994 to 54 percent in 2009—and although it is very difficult to estimate total sales for this sector (Deconinck 2020), these figures do indicate the scale of changes in such a short period. The ETC Group estimates that in 2020 four firms controlled approximately 51 percent of seed sales, and that these same four firms accounted for more than 62 percent of global agrochemical sales (see figures below).

The global digital agricultural industry

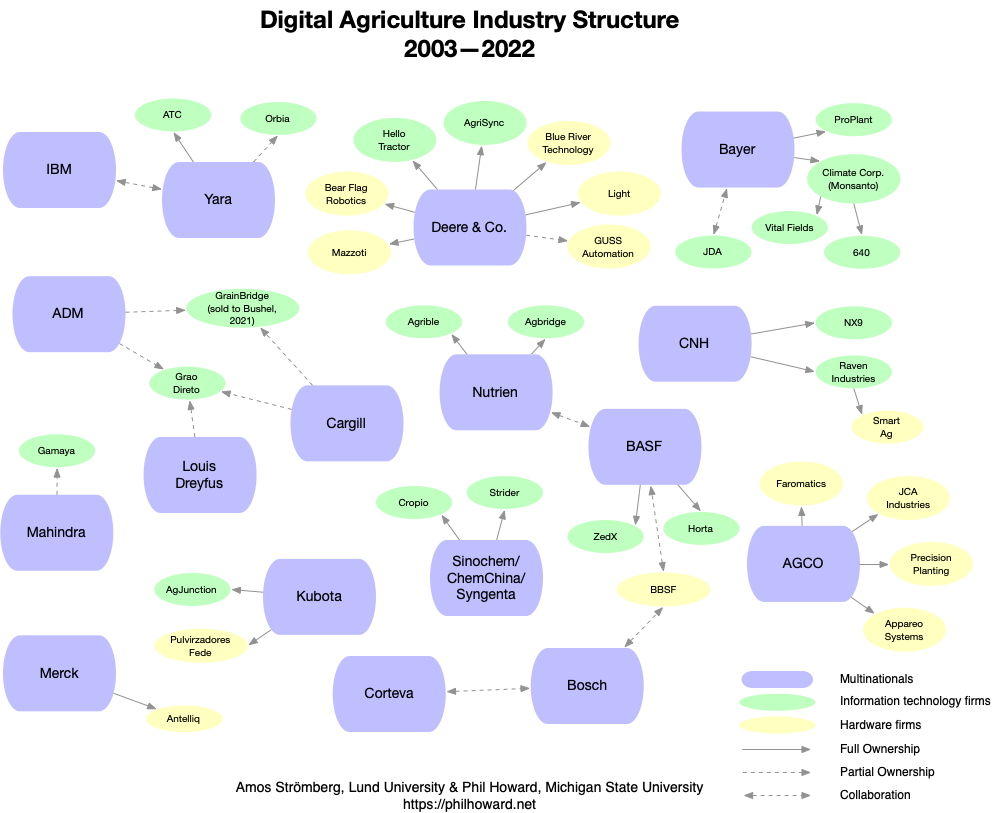

Kelly Bronson, in The Immaculate Conception of Data (2022: 18), suggests “the site of power in the food system has moved from seed and chemicals (or seeds paired to be useful only with chemicals) to data.” For this reason, we also explored ownership changes in digital agricultural industries. Following an unprecedented use of data-related technologies in farming, also referred to as “smart farming” or “the fourth agricultural revolution”, the agricultural sector has witnessed tectonic shifts in the recent years. Ever since Monsanto (before its acquisition by Bayer) made a ground-breaking purchase of The Climate Corporation for $930 million in 2013, many corporate giants have followed suit, showing a surging interest in digital agriculture. Executives at agricultural machinery firm John Deere, for example, said they want to “build a world of fully autonomous farming by 2030”, and Dan Rykhus, CEO of precision agriculture company Raven Industries, is certain that autonomous machinery is “the future of farming”.

As a result, many giant companies that previously have not been involved in food production, such as Google, Microsoft, Amazon and Bosch, now penetrate the agricultural sector, offering farmers a variety of technological tools such as automatic tractors, satellites, Internet of Things (IOTs), and a myriad of apps and software (Birner 2021). Consequently, companies hope to make use of “big data, artificial intelligence, and automation along the entire commodity chain, from input production and harvesting, packaging, transportation and consumption” (Hackforth 2021: 1). Moreover, the harnessed agricultural data will allow for higher levels of surveillance and enable agribusiness to tailor advertisement packages to farmers (Bronson 2022). This has led to concerns that digital agriculture will only exacerbate existing inequalities, including between core- and peripheral nations, urban and rural areas, ethnic majorities and minorities, and men and women (Birner 2021). In addition, these trends are contributing to lock-ins, or a tendency to make industrial farming systems even more resistant to change—such as by increasing the cost of switching to other data platforms, steering users toward more expensive inputs and larger-scale operations, or steering users away from crops other than commodity corn and soybeans (Bronson 2019; Carolan 2020; Ryan 2020)

Two key trends are multinational agricultural input companies investing in the digital market (e.g., Syngenta’s acquisition of leading digital platform company The Cropio Group in 2019), or collaborating with large multinational software companies (e.g., Microsoft signing larger deals with Bayer in 2021). But we also see non-agricultural hardware companies such as engineering firm Bosch starting to develop machinery suitable for digital agriculture (Birner et al. 2021). In addition, there are hundreds of smaller start-up companies entering the scene, such as Silicon Valley based Bear Flag Robotics, which was acquired by Deere for $250M in 2021. Some of these transactions involved substantial sums, such as when CNH Industrial bought Raven Industries in 2021 for $2.1B.

Update: January 2023, Google/Alphabet invested in Cropin and announced a startup called Mineral.

Malthusian justifications

One of the most notable conclusions to be drawn from the latest trends within agricultural input industries is the continued consolidation of power, and expectations from investors that these trends will not slow down in the near future. While the dominant agribusiness firms and proponents of digital agriculture assert that smart farming and industry consolidation will be needed to increase the amount of food needed to feed a growing world population, this is a smokescreen. Glenn Davis Stone, in The Agricultural Dilemma. How Not to Feed the World (2022), details how Malthusians have it exactly backwards—the real problem is overproduction due to massive government subsidies (particularly agricultural input industries), which leads to a “runaway train” of industrial agriculture, not population growth.

References

Baran, Paul A., and Paul M. Sweezy. 1966. Monopoly Capital: An Essay on the American Economic and Social Order. New York: Monthly Review Press.

Bronson, Kelly. 2019. Looking through a Responsible Innovation Lens at Uneven Engagements with Digital Farming.” NJAS—Wageningen Journal of Life Sciences, 90–91: 100294.

Bronson, Kelly. 2022. The Immaculate Conception of Data. McGill-Queen’s University Press.

Birner, Regina, Thomas Daum, and Carl Pray. 2021. Who Drives the Digital Revolution in Agriculture? A Review of Supply-Side Trends, Players and Challenges. Applied Economic Perspectives and Policy 43. 10.1002/aepp.13145.

Carolan, Michael. 2020. Acting Like an Algorithm: Digital Farming Platforms and the Trajectories They (Need Not) Lock-In. Agriculture and Human Values 37, 1041–1053.

Deconinck, Koen. 2020. Concentration in Seed and Biotech Markets: Extent, Causes, and Impacts. Annual Review of Resource Economics 12(1),129-147.

ETC Group. 2022. Food Barons 2022: Crisis Profiteering, Digitalization and Shifting Power. Available at: https://www.etcgroup.org/files/files/food_barons-summary-web.pdf.

Fuglie, Keith, Paul Heisey, John L. King, Kelly Day-Rubenstein, David Schimmelpfennig, Sun Ling Wang, Carl E. Pray, and Rupa Karmarkar- Deshmukh. 2011. Research Investments and Market Structure in the Food Processing, Agricultural Input, and Biofuel Industries Worldwide. Economic Research Report—130. Washington, DC: USDA Economic Research Service.

Howard, Philip H. 2009. Visualizing Consolidation in the Global Seed Industry: 1996–2008. Sustainability 1(4), 1266-1287.

Howard, Philip H. 2021. Concentration and Power in the Food System. Who Controls What We Eat? Revised Edition. London: Bloomsbury Academic.

Hackfort, Sarah. 2021. Patterns of Inequalities in Digital Agriculture: A Systematic Literature Review. Sustainability 13(22), 12345.

Ryan, Mark. 2020. Agricultural Big Data Analytics and the Ethics of Power. Journal of Agricultural and Environmental Ethics 33 (1): 49–69.

Scherer, Frederic M., and David Ross. 1990. Industrial Market Structure and Economic Performance. 3rd ed. Boston, MA: Houghton Mifflin Company.

Shepherd, William G., and Joanna M. Shepherd. 2004. The Economics of Industrial Organization. 5th ed. Long Grove, IL: Waveland Press.

Stone, Glenn Davis. 2022. The Agricultural Dilemma. How Not to Feed the World. New York: Routledge.

10 thoughts on “Recent Changes in the Global Seed Industry and Digital Agriculture Industries”