Phil Howard, Terra Bogart, Alix Grabowski, Rebecca Mino, Nick Molen & Steve Schultze

Michigan State University, December 2012

No other section of the supermarket offers as many choices as the wine aisle. A typical retailer is likely to have hundreds of unique wines on its shelves. Just three firms, however, account for more than half of the wine sales in the United States. What impact does this industry concentration have on consumer choices? To answer this question we conducted an inventory of wine offerings at 20 retailers in Michigan. We recorded more than 3,600 unique varieties of wine, and traced their relationships with more than 1,000 different firms. The graphic linked below shows the 1,892 brands owned, licensed or exclusively imported by these firms (click to enlarge).

Despite this incredible degree of choice on the shelves, wine sales are dominated by a much smaller number brands, and an even smaller number of firms, as the graphic below shows (click to enlarge).

PDF version of U.S. Wine Market Share, 2011

This retail landscape is not as concentrated as beer and soft drinks, particularly at the brand level, as leading products in these categories (Bud Light, Coors Light, Coke, Pepsi, etc.), can be found at almost every store. In contrast, the only unique varieties of wine found in more than half the retailers in our inventory were Clos du Bois chardonnay (Constellation Brands) at 13 out of 20 stores, and Cavit pinot grigio (Cavit) at 11. Half of the stores carried the following six varieties:

Constellation Brands

Blackstone merlot

Ravenswood zinfandel

Woodbridge chardonnay

E & J Gallo

Apothic red

Barefoot chardonnay

Ecco Domani pinot grigio

The vast majority of varieties were far less common, with 72.8% recorded in only one store, and 87% in two or fewer stores.

The figures below show selected results for other information we recorded in our inventory. They refer to unique varieties found on the shelves (not to sales figures or the amount of shelf space they occupy). Note that the top six firms, which are the same as the top six by U.S. sales, accounted for 21.9% of the total inventory (794 unique varieties).

Inventory of 20 Michigan retailers (n=3,626)

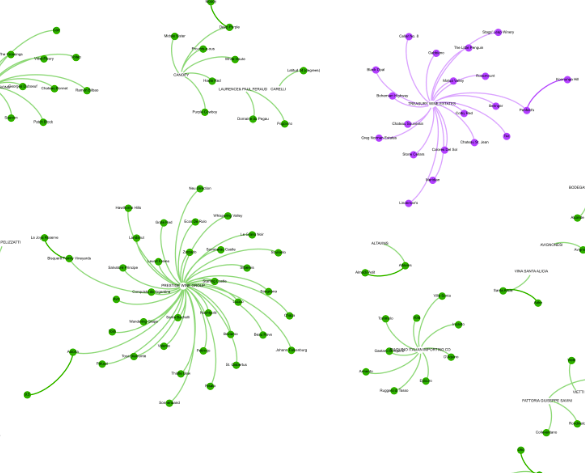

The top firms each contribute to an illusion of diverse ownership by offering dozens of brands (and hundreds of varieties), many of which do not clearly indicate the parent company on their label. The graphic below, for example, shows some of the more than 200 brands offered by the five largest wine firms in the U.S.

PDF version of The Top Five U.S. Wine Firms and Their Brands

Even company websites may not make ownership apparent. To give just one example, “Octavin Home Wine Bar” is in smaller print on a number of boxed wine brands, including Silver Birch (New Zealand), Pinot Evil (Hungary) and Herding Cats (South Africa). If you go to the Octavin website you’ll see it is a trademark of Underdog Wine & Spirits. If you then go to the Underdog Wine & Spirits website and make the effort to go to the “about” page, you will see in the fine print that it is a unit of The Wine Group, the second largest wine company in the U.S. (hardly an “underdog”).

We found the illusion of diverse ownership to be strongest at chain drug stores. CVS and Rite Aid each offered more than one hundred unique varieties, but the majority were supplied by E. & J. Gallo or Constellation Brands, and fewer than 20 firms were represented on the shelves. It was weakest at local retailers with extensive wine selections. One wine shop we visited offered products from 446 different firms, and no firm represented more than 2.6% of the varieties.

Part of the reason wine remains far less concentrated at the brand level when compared to beer and soft drinks is that wine distributors do not usually stock the shelves directly, and stores have retained more control over their selections. Many retailers rely on “category captains,” or staff from beer and soft drink distributors (which carry products primarily from one producer) to plan the alignment of all of these beverages on their shelves.

Another reason for so many brand choices among the top firms is that wine has a much larger price range than other beverages. A single company may offer products in niches that range from inexpensive boxed wines on the bottom shelves, to $100+ bottles on the top shelves. Interestingly, Constellation Brands’ recent strategy to increase profitability is to focus on offering higher-priced, premium wines. This firm sold its lower-priced brands Almaden, Inglenook and Paul Masson to The Wine Group in 2008. Constellation also announced in June 2012 that it would be introducing more than 50 new brands and line extensions during the year.

Although it is not at the same level as the beer and soft drink industries (where two firms control approximately three-quarters of all sales in the U.S.), the wine industry is becoming more concentrated. A large number of acquisitions and mergers have taken place in the past decade, such as Constellation Brands acquisitions of Mondavi ($1.3 billion in 2004), Vincor ($1.3 billion in 2006) and Fortune Brands’ wine business ($885 million in 2007). Although choices remain abundant, particularly for those with access to non-chain retailers, it is increasingly difficult for consumers to recognize which companies they are supporting with their purchases.

For additional aspects of this study see:

Wine Labeling, by Alix Grabowski

The Availability of Michigan-Produced Wines in Southern Michigan Retail Locations, by Rebecca Mino

Methods

We conducted inventories of wine at 20 retailers in Michigan in March and April 2012. We recorded every variety of wine, but excluded fortified wines (e.g. port, sherry), non-alcoholic wines, and wines without any grape juice (e.g. 100% cherry wine). Varieties available in multiple sizes were only counted once. The retailers included:

Aldi

World Market

CVS

Kroger

Meijer

Rite Aid

Sam’s Club

Target

Trader Joe’s

Walgreen’s

Walmart

Whole Foods

one local convenience chain

two local wine shops

two local supermarkets

three local natural food stores

Most retailers were located in the Lansing metropolitan area. Because this part of the state does not have Trader Joe’s or a Whole Foods we traveled to Detroit and Ann Arbor to inventory stores that were part of these chains. The number of varieties recorded at each retailer ranged from a low of 31 at Aldi, to a high of 840 at a local supermarket. The total for all stores was 5,753, with a mean of 288 unique varieties per store. Ownership/licensing/exclusive importer information was identified through company websites, trade publications and trademark databases. Information graphics were created with Gephi, Many Eyes, Inkscape and OmniGraffle.

Further Reading

Veseth, Mike. 2011. Wine Wars: The Curse of the Blue Nun, the Miracle of Two Buck Chuck, and the Revenge of the Terroirists. Rowman & Littlefield Publishers.

Colman, Tyler. 2008. Wine Politics: How Governments, Environmentalists, Mobsters and Critics Influence the Wines We Drink. University of California Press.

Author Affiliations

Phil Howard,1 Terra Bogart,1 Alix Grabowski,2 Rebecca Mino,1 Nick Molen3 & Steve Schultze3

1. Dept. of Community, Agriculture, Recreation & Resource Studies 2. Dept. of Packaging 3. Dept. of Geography

Appendix

A spreadsheet with a list of the wines and varieties in our inventory, along with origin and ownership/licensing/exclusive importer data is included here. Use the find tool in your web browser to look up specific brands or firms.

One thought on “Concentration in the U.S. Wine Industry”