Phil Howard and Ginger Ogilvie

August, 2011

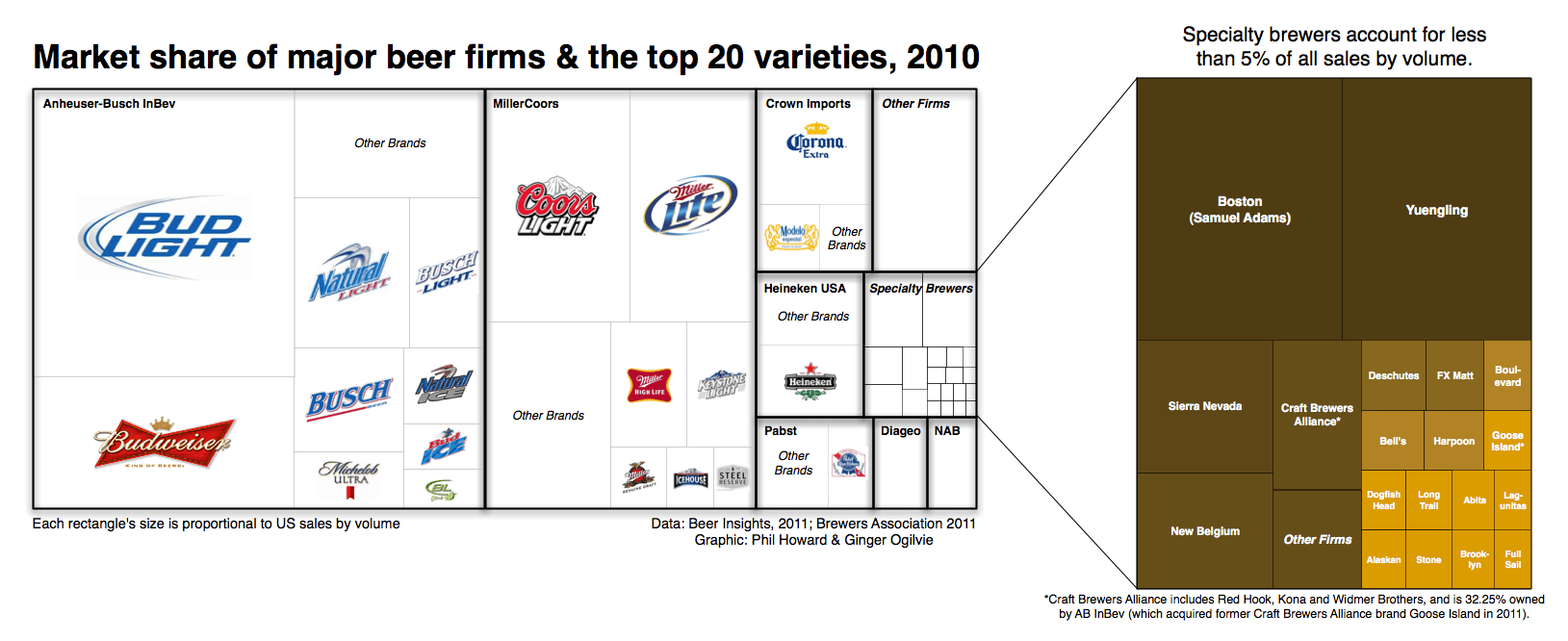

There is an appearance of great diversity in the number of brands and varieties of beer sold in the United States. The beer industry, however, is dominated by a relatively small number of firms.

AB InBev owns, co-owns or distributes more than 36 brands, for example, while MillerCoors controls at least 24 more. MillerCoors also brews Metropoulos & Company’s products under contract (thus the company that controls Pabst and 21 other brands is a “virtual” beer company).

Larger version of Ownership of Beer Brands and Varieties, 2010 (PDF, 1.2MB) [note that the graphic above focuses on the top 13 firms, and excludes varieties of malt liquor and non-alcoholic beers]

Increasing Concentration after World War II

In 1959 the 10th largest brewery in the country (Pabst) acquired the 18th largest brewery (Blatz), resulting in a combined national market share of 4.5%. Seven years later the US Supreme Court reversed the merger, noting that:

If not stopped, this decline in the number of separate competitors and this rise in the share of the market controlled by the larger beer manufacturers are bound to lead to greater and greater concentration of the beer industry into fewer and fewer hands [1].

Today, just two firms control more than three-quarters of all sales.

(click for larger version) The beer industry is not only dominated by two firms, it is dominated by a small number of varieties – just six account for more than half of all sales. The result is an “oligopoly within the oligopoly” [2].

The Rise of Small Breweries Since the 1980s

The number of breweries has increased rapidly since 1983, when there were fewer than 50 in the US, to 1,828 by 2010. The vast majority (93%) are brewpubs or microbreweries, however, with tiny market shares. They tend to concentrate geographically in the northern half of the US.

Global Trends

The fears of the Supreme Court Justices of the 1960s have been realized, but are unlikely to be reversed in the near future, despite the rapid growth of small breweries. This is true not only for the US, but worldwide, as the top four firms increased their global market share from 22% in 1998 to almost 50% in 2010. AB InBev, MillerCoors, Heineken (headquartered in The Netherlands) and Carlsberg (headquartered in Denmark) also account for approximately two-thirds of global industry profits [3].

Literature Cited

1. Justice Hugo Black in U.S. v. PABST BREWING CO., 384 U.S. 546 (1966). Quoted in “Is Big Beer begging for an antitrust probe?” by Aliza Rosenbaum and Rob Cox, The Washington Post, September 6, 2009.

2. Hannaford, Stephen G. 2007. Market Domination!: The Impact of Industry Consolidation on Competition, Innovation and Consumer Choice, p. 122. Westport, CT: Praeger.

3. The Economist. 2011. The global beer industry. May 5.

See also: Howard, Philip H. Too Big to Ale? Globalization and Consolidation in the Beer Industry. Pp. 155-165 in The Geography of Beer: Regions, Environment, and Society (Mark W. Patterson & Nancy Hoalst Pullen, eds.). New York: Springer. [pre-publication PDF]

{kind=link}

One thought on “Concentration in the U.S. Beer Industry”