Summary: Big brewers, which have experienced declining sales for their beer brands in the last decade, have been accused of “craftwashing” by some craft brewers and their aficionados—they define craftwashing as big brewers (>6 million barrels per year) taking advantage of the increasing sales of craft beer by emulating these products or by acquiring craft breweries, while also obscuring their ownership from consumers. To estimate the prevalence of these practices, the ownership of U.S. mainstream and craft beer brands was decoded and visualized. In addition, an exploratory case study analyzed how these ownership relations are represented in the craft sections of selected retailers (n = 16) in the Lansing, Michigan metropolitan area. By October 2017 in the U.S., all but one big brewer had either acquired a craft brewery, or formed a distribution alliance with one—without disclosing these relationships on the packaging. In the study area, 30% of 4- and 6-pack facings recorded in craft beer sections (n = 1145) had ownership ties to big brewers. Craftwashing is common in the U.S. beer industry, and this suggests consumers must exert substantial effort to become aware of their own role in reinforcing these practices.

An initial craftwashing strategy was launching “faux craft” or “crafty” beers, with the production of these products by big brewers kept relatively hidden. The packaging, placement, and even the price of these beers leads typical consumers to believe that they are purchasing an independently owned craft beer. One example is Anheuser-Busch InBev’s (Leuven, Belgium) brand Shock Top: an internal document in 2014 touted data indicating 75% of consumers thought it was from a small brewer, and highlighted the line, “Shock Top is (AB InBev subsidiary) Labatt’s big bet in the battle against Micro Craft.”

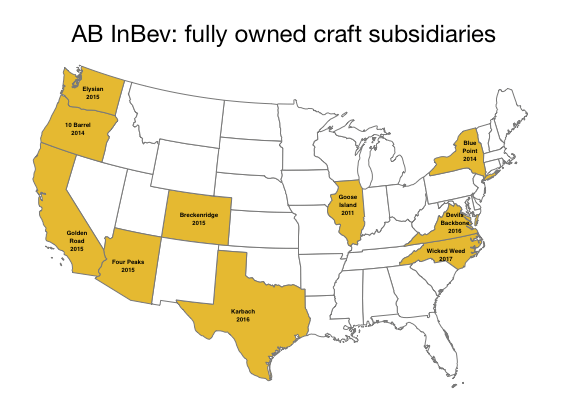

The “crafty” strategy, however, encountered slower sales in recent years, such as an estimated 4% decline for Molson Coors’ (Denver, CO, USA) brand Blue Moon and 9% decline for Shock Top in 2016. As a result, a more recent strategy is the acquisition of successful craft breweries by big brewers. AB InBev, for example, has acquired ten craft brewers in the U.S. in the last seven years, as shown in the map below, and has partial stakes in five more. Ownership ties to the new parent corporations are also typically not disclosed, even as the big brewers’ resources enable the distribution and marketing of newly acquired brands to increase dramatically.

Geography of craft acquisitions made by Anheuser-Busch InBev in the United States, 2011 to 2017.

Craft brewers, particularly those organized in the Brewers Association (Boulder, CO, USA), have been increasingly vocal in their displeasure with these actions. They point out the numerous efforts big brewers have engaged in to keep independent craft brewers off the shelves of retailers and distributors, as well as to discourage consumers from buying their products. Just a few examples include:

-

One of the two leading beer firms is frequently designated by retail chains as the “category captain”, which gives them the power to design the placement and allotted shelf space for the entire beer section, including direct competitors’ products.

-

After an investigation, the Department of Justice prohibited AB InBev from “continuing practices and programs that disincentive distributors from selling and promoting the beers of… rivals.”

-

AB InBev ran advertisements during the 2015 and 2016 Super Bowls belittling craft beer drinkers.

Although the U.S. government has not yet intervened in craftwashing disputes, there have been several private lawsuits accusing big brewers of deceptive marketing for “import” brands that are actually brewed in the U.S. (one against AB InBev brand Beck’s was successful). In Australia, however, the largest brewery was fined approximately US $18,000 by a government agency, and agreed to stop distributing its “Byron Bay Pale Lager”. The regulators said the packaging on the Carlton & United (now a division of AB InBev) beer had deceived consumers into thinking it was made in a small facility, far from the industrial-scale brewery where it was actually produced. Jim Koch, the founder of Boston Beer Co., (Samuel Adams) (Boston, MA, USA) has said, “I think a beer drinker shouldn’t have to hire a private detective to figure out who actually makes the beer that they’re drinking”—although it should be pointed out that he engaged in a very similar practice with the “Oregon Beer and Brewing Co.” (Salem, OR, USA) in the 1990s.

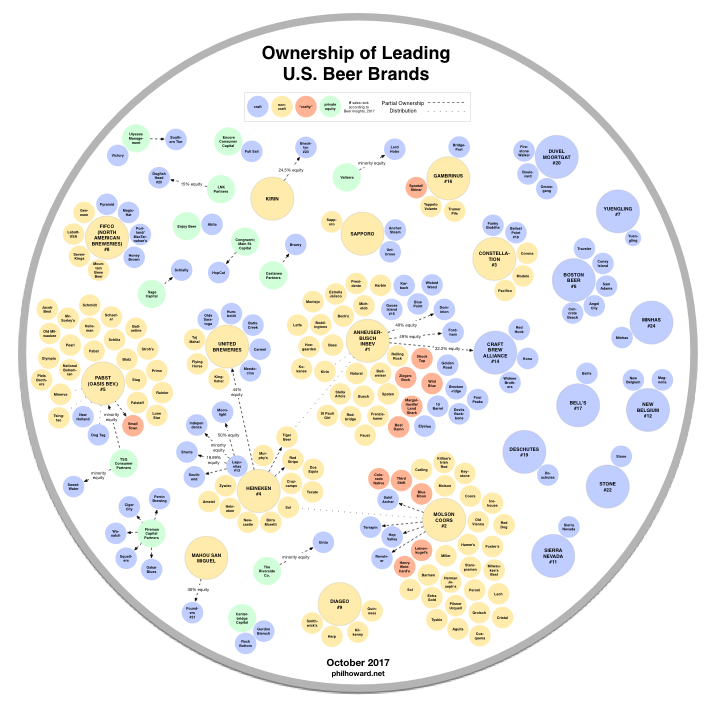

In response to craftwashing, the Brewers Association, which represents small and independent brewers in the U.S., released an “independent craft” seal in June 2017. Members and eligible non-members can place this seal on their beer labels, to help consumers identify which breweries do not have hidden ownership ties. To qualify, a brewery must produce 6 billion barrels or less annually, and have less than 25% ownership by a larger beer/wine/spirits firm. Under this definition, craft brewers that sell ownership stakes to private equity firms remain eligible for membership. The goals of private equity firms, however, are typically to achieve returns of 25–100% compounded annually, and a payout within three to seven years, which increases the likelihood that these breweries will eventually be sold to larger firms. One of the largest members of the Brewers Association, Boston Beer, is publicly traded, and is therefore also susceptible to takeover attempts by larger firms.

For updates see Recent Changes in the U.S. Beer Industry

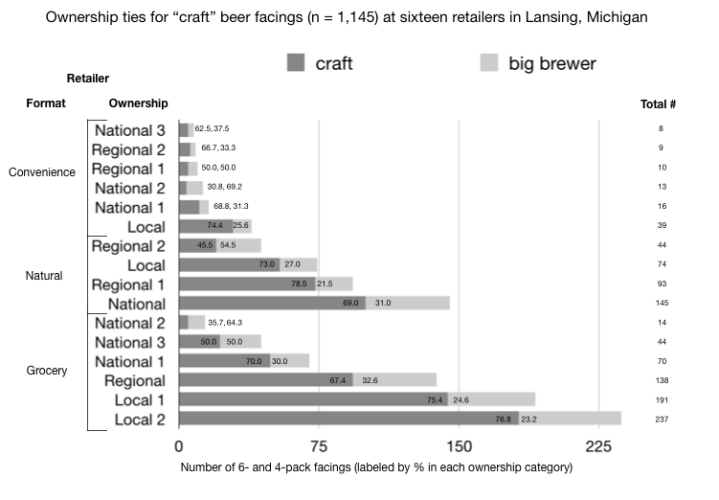

The bar chart below shows the results of an inventory of 4- and 6-packs shelved within craft beer sections at 16 retailers in the Lansing, Michigan area (October 2017). The figure is organized as ascending from the smallest to largest number craft beer facings in each of three retailer formats. As expected, these formats had strong differences in the number of craft facings, due to more limited shelf space at convenience stores, in comparison to natural food stores and mainstream grocers. Convenience stores offered 8 to 39 craft offerings, with the locally-owned store offering the most facings in this format. There was more variation in shelf space devoted to craft beer at natural and grocery formats: as low as 14 craft facings at one nationally-owned grocery retailer, and as high as 237 at one locally-owned grocery retailer. The average number of facings for all 16 retailers was 71.5.

The average percentage of craft facings with ownership ties to big brewers was 37.9% when calculated at the retailer level (i.e., not for the total number of facings in the study). Locally-owned retailers had percentages in a relatively narrow range, from 21.5% (natural) to 25.6% (convenience). Regionally and nationally-owned retailers all reported higher percentages, and their facings with big brewer ties ranged from 30.0% (grocery) to 69.2% (convenience).

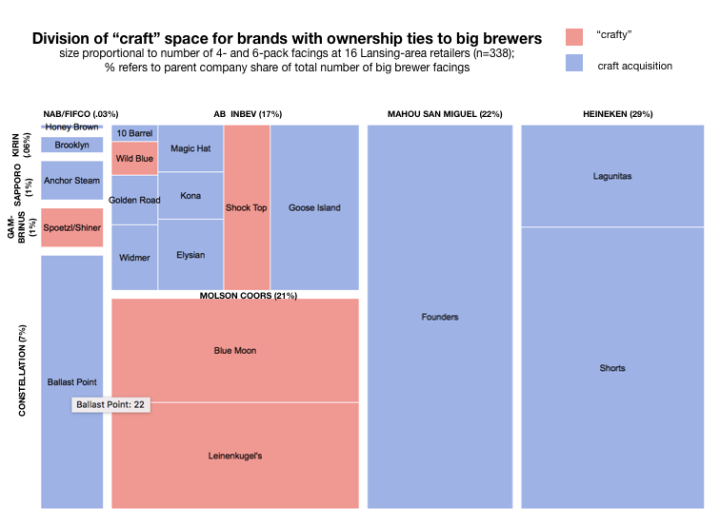

For the sample as a whole, 30.0% of the 1,145 facings were fully or partially owned by big brewers. The treemap below illustrates the breakdown of the study shelf space that was coded as “craftwashing,” divided by parent firm, and subdivided by their brands. The brands with the highest percentage of facings were Michigan-based breweries Founders and Shorts (approximately 22% each). However, Molson Coors’ “crafty” brands Blue Moon and Leinenkugel’s also take up a significant amount of space in the region’s craft beer sections (21%), although none of Molson Coors’ recently acquired brands were recorded in the study area. Conversely, AB InBev’s recent craft acquisitions took up substantially more shelf space than their “crafty” offerings (Shock Top, Wild Blue). Constellation has also been quite successful in placing a California-brewed acquisition on this area’s shelves (11%), after paying $1 billion for Ballast Point’s craft brewing and distilling operations in November 2015.

The results suggest that craftwashing in the U.S. beer industry is quite widespread, with only one big brewer (Diageo) so far resisting craft acquisitions. It is difficult for a typical consumer to identify ownership ties with big brewers, both for “crafty” brands and those with formerly independent craft heritage. The large numbers of acquisitions by private equity firms in recent years suggests that even more independent craft breweries will eventually be acquired by big brewers or other large corporations. As a result, those who want to support independent craft brewers must exert substantial effort to remain fully informed, and avoid unintentionally reinforcing these trends.

Big brewers have shifted from crafty introductions to acquiring brands with craft heritage. This change was influenced by the lack of effectiveness of the crafty strategy—the craft segment continues to grow, and at the expense of big brewers’ total sales. The situation is very dynamic, however, and the largest independent (or “mass craft”) breweries, such as Boston, Sierra Nevada, and New Belgium, have also experienced flat or declining sales in recent years. Much of the growth in the craft segment is now concentrated at the smaller-scale, such as neighborhood micro-breweries. This has coincided with the rise of consumer “neolocalism”, or loyalty to local place identities. A rapidly increasing number of craft brands are entering the U.S. market, but the amount of craft shelf space at retailers is remaining relatively static. As a result, retailers’ definitions of what is craft beer and what is not, will be a key factor in influencing how craftwashing strategies evolve in new directions.

For more details see: Howard, Philip H. 2018. Craftwashing in the U.S. Beer Industry. Beverages 4(1), 1.

3 thoughts on “Craftwashing in the U.S. Beer Industry”